In brief:

- Risk is becoming a defining factor for fashion, reshaping supply, cost structures and day-to-day decisions

- Nature-related risks remain under-addressed and are not yet fully reflected in business decision-making

- Most companies assess risk at a high level, but struggle to translate insights into actionable, financial terms

- Adaptation and supplier engagement remain limited, despite being critical to maintaining performance

- Companies that move from assessment to action can unlock near-term value while strengthening long-term resilience

Risk is the new reality for fashion

For years, the assumption within the fashion industry was that more sustainable products would drive demand and differentiation. That hasn’t materialized at scale. Growth in ultra-fast fashion continues to outpace more sustainable alternatives, and consumer interest hasn’t consistently translated into purchasing decisions. As a result, demand is becoming a less reliable driver, and attention is shifting to how the business operates and where it’s exposed.

Fashion depends on biodiversity for raw materials, water for processing and land for production. Over time, sourcing has concentrated around a limited set of materials and regions, reducing resilience and increasing exposure to disruption.

Today, risk is now emerging across materials, suppliers and cost structures — affecting availability, price and input quality — and most companies are not yet fully prepared to manage it.

Where companies stand today

Many companies have made progress on climate risk, while nature-related risks remain under-addressed and not yet fully reflected in business decisions. Most organizations still lack visibility into how ecosystem dependencies — such as soil health, water availability and biodiversity — affect cost, availability and performance, particularly across complex, global supply chains. Far fewer have integrated environmental risk fully within their enterprise risk management (ERM) systems.

To better understand how companies are approaching this, we conducted an anonymous survey of fashion and sporting goods companies to assess how they are identifying and managing climate and nature-related risks.

Dependency on nature is still under-assessed and rarely built into decision-making, despite the emergence of frameworks such as the Taskforce on Nature-related Financial Disclosures (TNFD), The Corporate Sustainability Reporting Directive (CSRD), and the Science Based Targets Network (SBTN). This leaves companies increasingly exposed to supply disruption, cost volatility and operational risk.

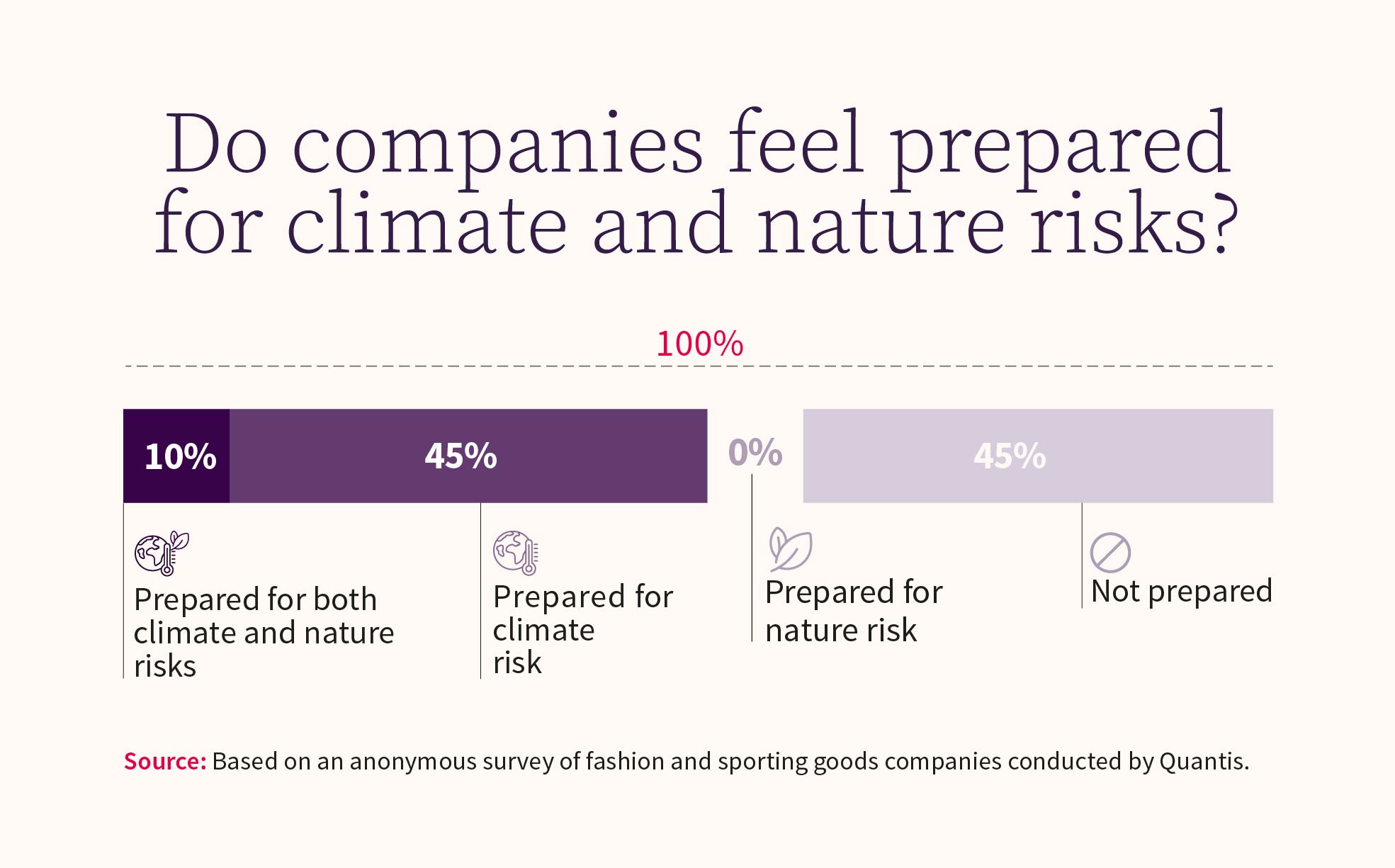

The results show a clear imbalance. While half of the surveyed companies report feeling some level of preparedness for climate risk, none report feeling prepared for nature-related risks alone — and only a small share feel equipped to address both together. This gap points to a critical opportunity to strengthen risk management by integrating climate and nature into a more cohesive approach.

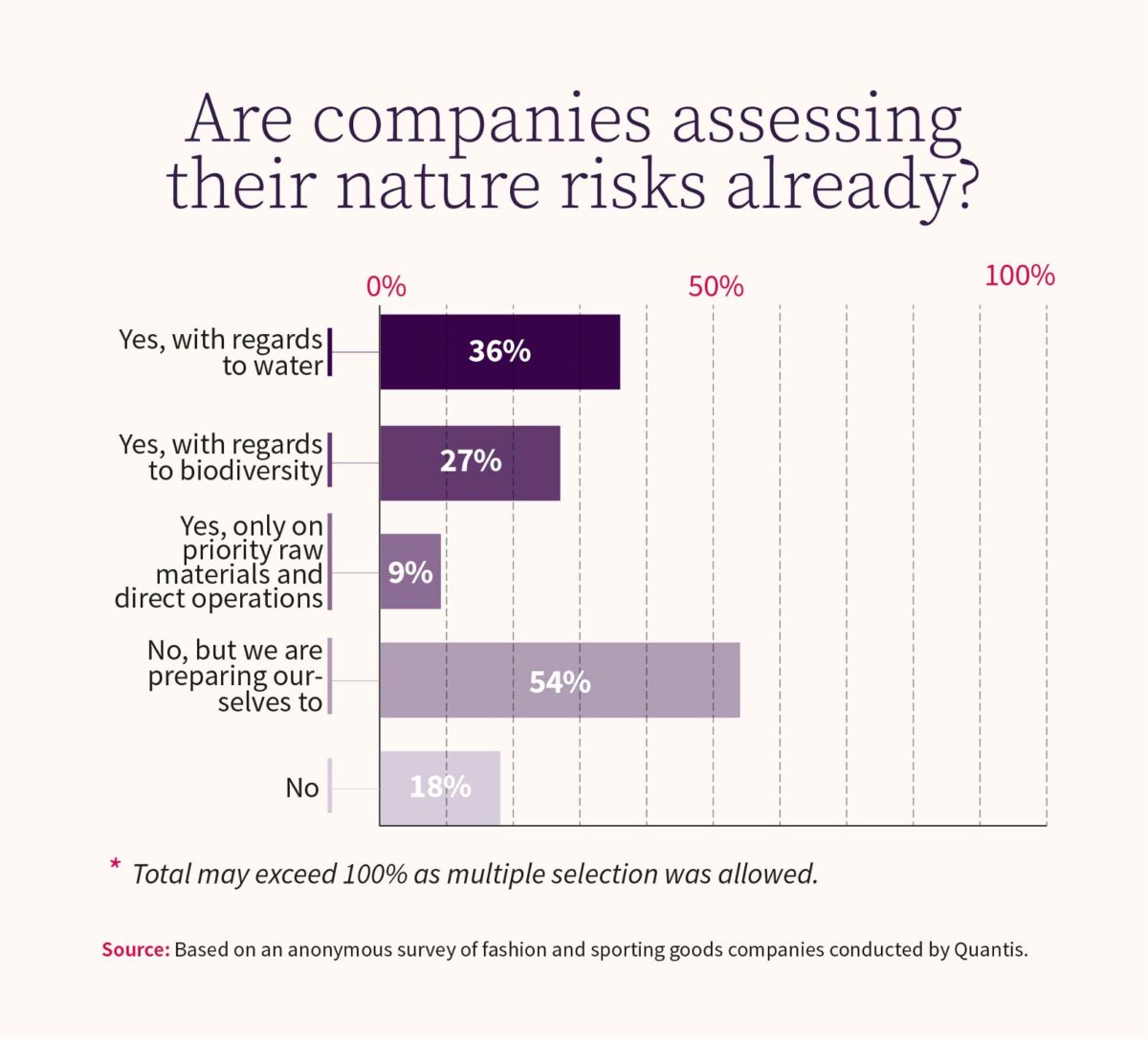

The approach varies for respondents that have started to address nature risk. Some are focusing on specific topics such as water or biodiversity, while others are still in early preparation stages. Few have a comprehensive view across materials and supply chains, where exposure is most concentrated.

At the same time, companies do not need to build entirely new approaches. Many of the systems, data and supplier relationships developed for climate can also be used to address nature-related risks. Integrating the two allows companies to expand scope and improve impact without duplicating effort. Because climate and nature risks are closely linked, progress in one area often strengthens the other, improving efficiency while building a more complete view of exposure.

From screening to decision-making

Most companies have started with qualitative risk assessment, using high-level screening to identify hotspots across materials and sourcing regions. This is a necessary step, particularly in upstream value chains where data is often limited.

However, in most cases, this work remains descriptive rather than decision-oriented. It identifies where exposure may sit, but does not yet determine how the business should respond.

Few companies are translating these insights into financial terms, linking environmental exposure to cost, margin or supply implications. Even fewer still are considering the cost of inaction, meaning their strategies are not future-oriented, as they’ve not yet considered how climate and nature will transform markets and reshape business models.

Without that translation, risk remains disconnected from the decisions that shape business performance. Sourcing strategies, supplier investments, and pricing decisions continue to be made without a clear view of how changing environmental conditions will affect outcomes. Even for companies who have done thorough risk analyses, the core challenge is bridging the gap between rich environmental assessment data and the companies’ integrated risk management taxonomy, scoring methodologies and governance forums. Fashion players need a scalable integration that enables consistent risk ownership, actionable responses and incorporation into strategic decision-making.

Adaptation is the real test

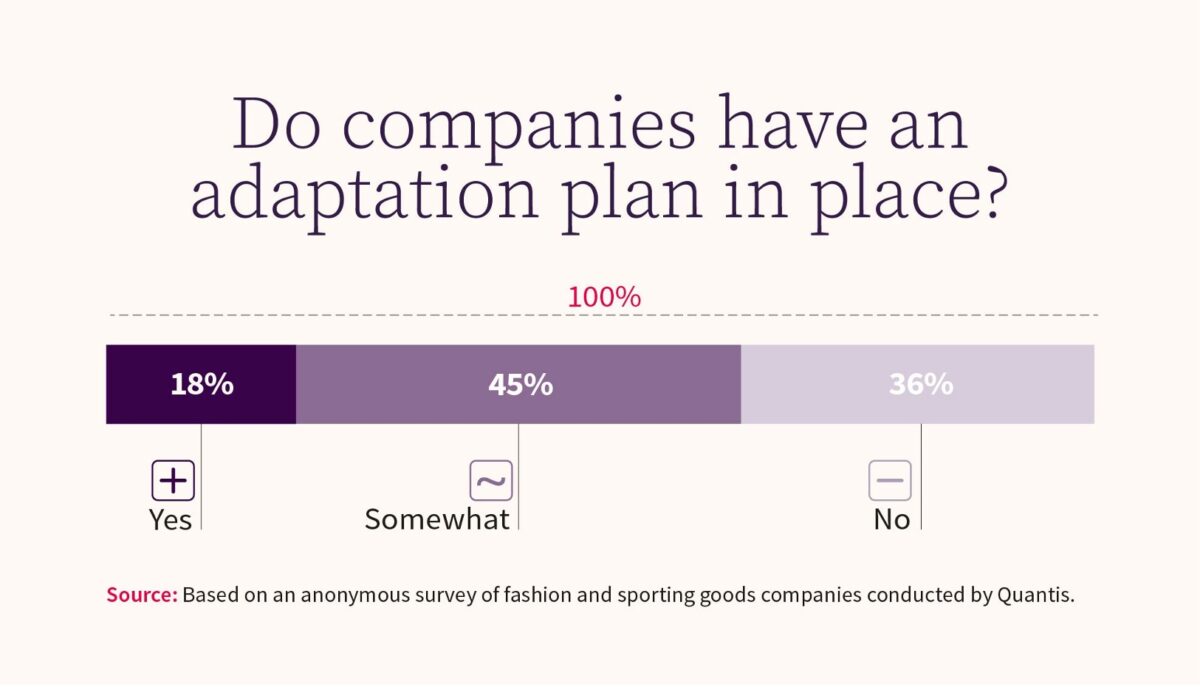

While many organizations have made strides in reducing emissions, far fewer have prioritized adaptation strategies that can meet regulatory expectations and withstand future shocks — a critical factor in ensuring resilience.

In practice, adaptation means adjusting sourcing, operations and supplier practices to perform under changing conditions, rather than reacting once disruption occurs.

For example, companies are starting to shift sourcing away from regions facing chronic water stress, support cotton suppliers in adopting irrigation and soil practices that stabilize yields, or diversify material inputs where climate exposure is concentrated. In manufacturing, this can mean reinforcing facilities in flood-prone areas or adapting production schedules to account for extreme heat.

These are not long-term ambitions — they’re near-term operational decisions that determine whether supply holds, costs remain stable and products reach the market.

Most companies have not yet reached this stage. Efforts tend to remain partial, with plans still in development or not yet defined. Even where action has started, it is often not coordinated across functions.

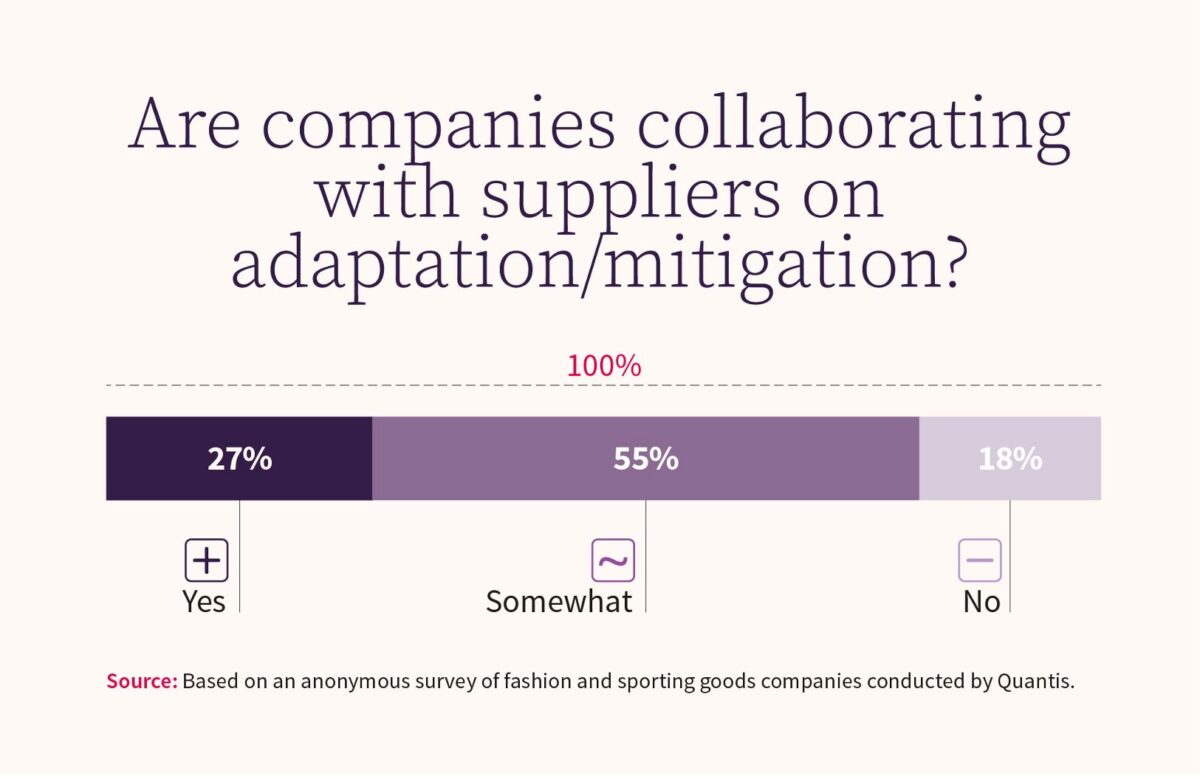

This is particularly visible in supplier engagement.

Some companies are beginning to work with suppliers, but collaboration is not yet consistent or embedded. At the same time, most are not engaging with the public sector — even though many risks, such as water stress or land degradation, extend beyond individual value chains and require coordinated responses.

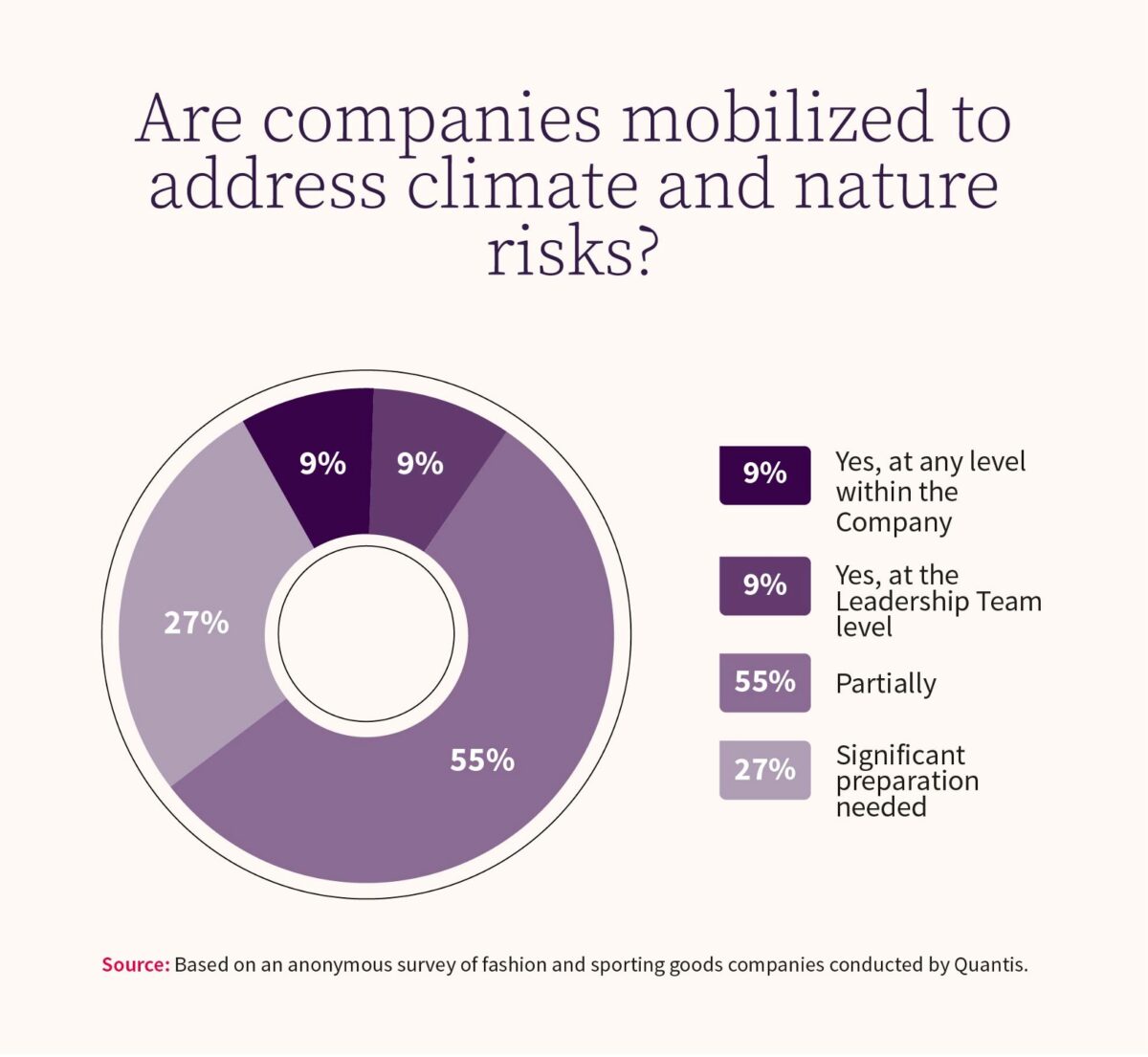

Mobilization remains limited

Even where risks are recognized, they are not yet fully integrated across organizations. One of the key reasons is that risk has not been financially quantified, making it difficult for leadership and operational functions to understand. Without translating risk into the language of different business functions, such as a clear business case for nature, the potential for action remains limited.

In many cases, responsibility sits within sustainability or specialist teams, rather than being shared across procurement, sourcing or finance. Only a small share of companies report full alignment at the leadership or enterprise level.

This limits the ability to act. Climate and nature risks affect core business functions, from material sourcing to cost structures and supplier stability, but are not yet consistently managed as such. Without leadership ownership, efforts remain fragmented and difficult to scale.

Supply chain partnerships: the role of Scope 3 in fashion

Most of fashion’s exposure sits outside direct operations, within Scope 3, across raw materials and suppliers in the value chain. This is where availability, cost and continuity are determined, and where disruption tends to emerge first.

Responding effectively requires more than visibility. Companies need data that is consistent, comparable and usable in decision-making.

Where progress is being made, it’s driven by closer supplier collaboration — aligning on priorities, supporting changes in practices and improving visibility across the value chain. These efforts take time and coordination, but they are essential to managing exposure at scale.

From risk to action

The focus now is execution. Addressing climate and nature risks means acting where they have the most direct impact, across materials, suppliers and cost.

Five priorities stand out:

1. Assess exposure across materials and supply

Map vulnerabilities from raw materials through production, including water, land and biodiversity factors at a local level. Prioritize depth over breadth — focus on hotspot materials, high-risk regions and critical suppliers to enable decision-making.

2. Link risk to financial impact

Translate exposure into cost, margin and supply implications to guide decisions.

3. Mobilize the leadership team

Climate and nature risks are business risks — affecting cost, supply and continuity. Treating them as a P&L issue ensures they are owned and acted on at the right level.

4. Embed climate and nature risk into sourcing, material strategy and enterprise risk management

Align sourcing with changing conditions. Manage existing materials, scale alternatives, and integrate environmental risks into enterprise risk management (ERM) systems to inform decision-making.

5. Strengthen supplier collaboration and decision systems

Work with suppliers to understand constraints, align on priorities and support adaptation.

What comes next for fashion

Risk is already reshaping sourcing, supplier relationships, and cost structures. Companies that act early will retain greater flexibility in how they respond — securing critical materials, supporting suppliers, and managing volatility as conditions evolve. Many fashion brands are already directly exposed to nature-related impacts across their operations, making the case for proactive risk assessment more immediate and tangible. When translated into the brand’s business context and language, these risks reveal not only long-term resilience needs but also significant short-term value and decision-making benefits.

Access the executive report

Download the executive report to understand how climate and nature risks are already shaping cost, supply and performance in fashion — and where to act now.