The release of the final SBTi Corporate Net-Zero Standard V2 on 11 June marks the end of a long and closely watched development process. Following the publication of two drafts in 2025, the update reflects extensive stakeholder input and debate on some of the most consequential questions in corporate climate target-setting: how companies set, deliver and report against net-zero targets, taking responsibility for ongoing emissions.

As with the previous versions, the Corporate Net-Zero Standard is a voluntary framework. However, V2 raises the bar beyond purely target setting, turning what was previously a commitment into an ongoing performance system, including transition planning, a performance-based 5-year target cycle to ensure targets reflect effective past progress and future ambition, and stronger reporting requirements operating on a best-effort basis and honest communication. The standard becomes more influential in shaping how companies design their climate journey, prepare for investor scrutiny, and meet disclosure and transition framework requirements.

Prefer to explore rather than scroll?

To allow companies to adapt to the material changes V2 introduces, the standard will be rolled out gradually:

- Until 31 January 2027: companies continue setting goals using V1.

- Between 1 February 2027 and 31 January 2028: both V1 and V2 can be used for target-setting, noting the SBTi recommends continuing to use V1 until the full application in February 2028.

- From 1 February 2028: New targets must follow V2, while existing targets are expected to remain valid until the end of their target timeframe or their 5-year cycle.

So what does this concretely mean for the 10,000 companies that have engaged with SBTi? Let’s look at the practical changes through five key questions:

- How does this impact my targets?

- How does this impact my roadmap?

- How does this impact my reporting and footprint measurement?

- Which sectors are most exposed?

- What should I do now vs later?

1. How does this impact my targets?

V2 fundamentally changes how targets are structured.

First, companies will define their base year based on the most recent footprint year instead of past base years (eg. 2018). Note that progress achieved under previous targets will be considered when defining the new ambition. Companies may also continue communicating progress relative to their original baseline externally, but official targets will reflect current emissions, ensuring ongoing alignment with net-zero pathways as the business evolves.

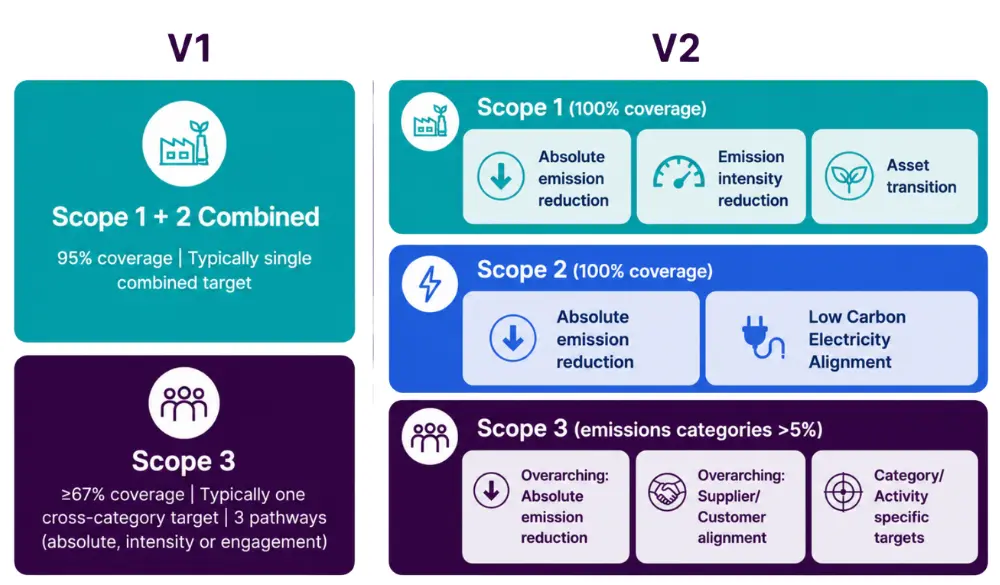

Beyond the base year, what was previously two targets, Scope 1 and 2 combined and Scope 3, now becomes a minimum of three: separate targets for Scope 1, Scope 2, and Scope 3, making each scope independently visible and accountable. Within each scope, the logic changes and targets can be further divided by category, activity or emission source, especially in Scope 3.

- Scope 1 now requires a 100% coverage of emissions and has three target-setting pathways available: absolute emissions reduction, emissions intensity reduction and asset transition.

- Scope 2 becomes standalone preventing Scope 1 transition delay, also requiring a 100% coverage and with two target-setting options available: absolute emissions reduction in line with the net-zero electricity pathway or low-carbon electricity alignment through high-credibility renewable procurement.

- Scope 3 target setting becomes more flexible with three approaches available, of which some can be combined: two overarching options — absolute emissions reduction covering all Scope 3 or supplier/customer alignment targeting tier 1 counterparties setting SBTs and one category-specific targets tailored per source. For the category-specific option, companies focus on significant categories (≥5% of total Scope 3), using quantitative targets for priority commodities/transport and alignment for other categories, while smaller sources remain excludable from target boundary.

The practical consequence: target-setting shifts from submitting a single commitment to managing separate targets for each scope — with companies able to choose for their Scope 3 targets between overarching approaches, providing broader options for mitigation or more granular category-specific targets on a subset of emissions based on their business priorities.

2. How does this impact my roadmap?

V2 brings target-setting closer to delivery planning. Under V1, the main focus was on the targets themselves, while the delivery plan remained unchecked. Under V2, companies are now expected not only to set targets, but also to deliver against those targets through a clear transition plan.

V2 also introduces an implementation hierarchy: companies must prioritize direct action (engaging suppliers, reducing at the source), then activity-pool actions (shared systems like grids, supply sheds) when direct action is not feasible, and finally sector-level actions when structural constraints exist.

SBTi target definition becomes less of a pure target-setting exercise and more of a transition management exercise. The key question is no longer only “what is our ambition?” but “what is our plan, what counts as progress, and how do we prove it?”

3. How does this impact my reporting and footprint measurement?

V2 makes measurement and reporting more structured, specific and auditable. The inventory coverage goes to 100%, removing the previously authorized 5% exclusion.

When it comes to the targets, Scope 1 and Scope 2 targets must cover 100%, but Scope 3 target boundary flexibility remains flexible for categories <5%. Companies also need to identify and quantify EIAs (Emissions-Intensive Activities).

Regarding disclosure, all companies must now publish their baseline emissions and targets within six months of validation. Category A companies must also publish their climate transition plan either at validation or within 15 months at the latest.

Furthermore, the annual progress reporting now goes beyond simply sharing the footprint evolution and performance. It requires companies to explain the barriers, gaps and corrective actions to ensure progress, and both the footprint and progress report is audited by a third party for Category A companies.

Reporting is no longer just about disclosure. It becomes how companies prove that their targets, transition plan and claims are credible over time.

4. Which sectors are most exposed?

While the Net-Zero Standard is cross-sectored, it will not affect all sectors in the same way. For some companies and sectors, it will mean a substantial redesign of targets, delivery plans, footprint measurement and reporting. For others, the changes may be more limited, especially for companies that have already made meaningful progress on decarbonization and will face a lighter transition.

Here are some key shifts for highly exposed sectors:

- Hard-to-abate industry (steel, cement, aluminum, chemicals): with Scope 1 requiring 100% coverage and available pathways, the focus will be on fossil transition, e.g. through Asset Decarbonization Plan, managing capex phasing and declining carbon budgets.

- Heavy electricity users (data centers, manufacturing): with Scope 2 aligned with electricity sector net-zero pathways and stricter integrity requirements, the focus shifts to upgrading renewable procurement strategies beyond basic RECs toward higher-quality certificates and/or PPAs.

- Diversified upstream Scope 3 (retailers, F&B, fashion): companies choosing the category-specific approach will have to build procurement-led strategies with granular supplier engagement at commodity level. Note that FLAG remains in application for ag value chains.

- Companies with material sold-product emissions (e.g. electronics, appliances): with product-use becoming an explicit target requirement, companies must integrate efficiency, phase-out and circularity into product strategy and R&D.

The overall direction does not change: credible action toward net-zero by 2050 at the latest, with companies expected not only to set targets, but also to act on them.

5. What should I do now vs later?

If you have valid targets through 2027 or beyond:

- Focus on delivering and achieving your current targets

- Understand V2’s requirements to prepare for eventual renewal

- Start building capabilities (cross-functional alignment, Scope 3 data systems, internal communication) that will ease transition when your targets come up for renewal

If you’re setting new targets soon:

SBTi recommends continuing with V1 and not delaying target-setting. V1 offers flexibility (combined Scope 1 and 2 targets, Scope 3 boundary options, lighter assurance) and your targets will remain valid for their full cycle; you will then transition to V2 for the subsequent cycle.

- Define and submit your targets using V1

- Prepare for eventual V2 transition by mapping your current targets against V2’s requirements (separate scope targets, implementation hierarchy, transition planning)

Over time: build the capabilities V2 will require, i.e. delivery planning, cross-functional alignment, and communication frameworks.

How Quantis can help

Quantis acts as your strategic partner, helping navigate V2 beyond technical interpretation.

We can support you in defining whether to adopt V2 now or phase in gradually, identifying financial and reputational implications of different pathway choices, and supporting board-level discussions on climate strategy evolution.

We help companies evaluate where V2 changes create risk versus opportunity — ensuring decisions on targets, capex allocation, and supply chain structures position you for long-term credibility while avoiding lock-in.

This article is also available as an interactive experience, navigate it at your own pace.